National CRE News In Your Inbox.

Sign up for Connect emails to stay informed with CRE stories that are 150 words or less.

The Old CRE Terms: They Ain’t What They Used to Be

The terms “gateway markets” and “core property types” are timeless commercial real estate categories. Gateway markets define major metropolises (think New York City, Boston, Washington D.C., Los Angeles, San Francisco and Chicago), while “core properties” tend to mean newer, Class A assets across the office, multifamily, industrial and retail property types.

However, MetLife Investment Management issued an interesting fact in a recently released report. “To our surprise, we found there has never been an authoritative methodology behind the commonly used real estate categorization of ‘gateway markets’ or ‘core property types,’” the MetLife IM analysts pointed out.

As a result, the report “Gateway Markets and Core Property Types: Not What They Used to Be” shed some light on the evolution of those gateway markets and core property concepts.

The History Behind the Terms

So, if there isn’t an official or authoritative methodology behind the terms, where did they come from?

MetLife IM Head of Real Estate Research and Strategy William Pattison told Connect CRE that the origins of the terminology can be traced to the 1980s and early 1990s. “To the best of our understanding, these were a way to guide institutional investors toward lower-risk segments of commercial real estate,” said Pattison, one of the report’s authors. He added that low risk was positively correlated to transparency at the time, which “favored office buildings and malls in the largest markets.”

The report pointed out that in the last two decades of the 20th century, metros like Chicago, New York City and Los Angeles tended to have the largest pool of available real estate investments. Furthermore, “because the markets and property types were so large, they were the only ones that had a semblance of transparency,” according to the report. As a result, this “made the risk profile seem more understandable.”

The Gateways of Today

Moving forward 20 years into the 21st century shows that things have changed with real estate. For example, given its historical price volatility, the report explained that Houston wouldn’t be considered a gateway market. But “given the size and magnitude of Houston’s industrial real estate, it could be justified as a ‘gateway industrial market,’” the report commented.

Pattison also indicated that cities like Atlanta, GA and Dallas, TX should be in the same category as Chicago and Los Angeles for investors interested in building a global real estate portfolio. Furthermore, “markets like Atlanta and Seattle now rank highly when we evaluate investment options using current performance datasets and factors unavailable when these terms were coined 40 years ago,” he said.

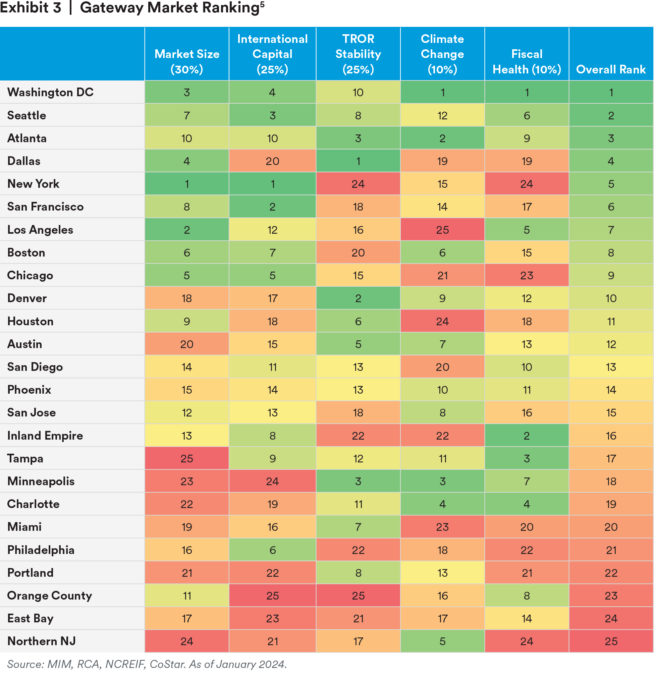

To that end, the report suggested five criteria to rank gateway markets:

- Market size

- International capital

- Total rate of return stability

- Climate change

- Fiscal health

Using the above factors, Washington, D.C., is ranked at the top of MetLife IM’s Gateway Market List, followed by Seattle, Atlanta, and Dallas. Trailing these top four are the generally accepted gateway cities of New York, San Francisco, Los Angeles, Boston and Chicago.

Expanding the “Core”

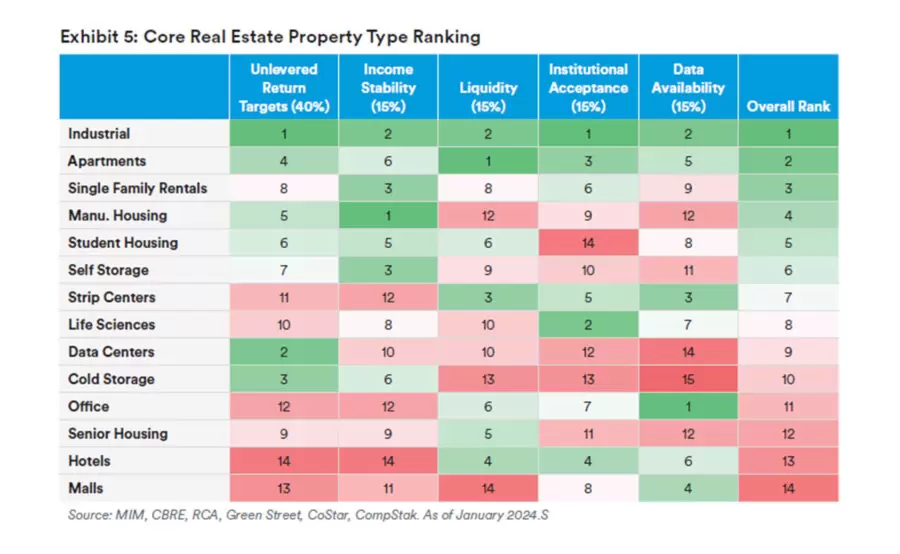

Once upon a time, “core” described the high-end trophy assets (primarily office and retail). But again, the available data has changed from 30 to 40 years ago. “Due to the maturation of the commercial real estate sector, we think that there should be more than just four core property types,” the report said. To that end, “core” should be defined by transparency, stable returns, income stability, liquidity, and institutional acceptance.

Under these standards, industrial takes top spot, while office is far down the list.

Within this new definition, “sectors like manufactured housing and single-family rentals now meet the criteria that should define ‘core’ property types,” Pattison pointed out. Furthermore, the previous definition of “core” focused primarily on visual appeal versus data. “With much more information available today, like decades of historical return performance, that approach is no longer sufficient,” Pattison said.

Changing the Mindset

Given the evolving world of commercial real estate, the report contended that the concepts of gateway markets and core property types should be reevaluated every five years.

“Labels shape investment decisions, and bad labels lead to bad portfolios,” Pattison said, explaining that the report’s goal was to help investors and managers think critically about how they measure and frame portfolio holdings and strategies. “Better classification and greater transparency should result in more optimized portfolios for the entire industry,” Pattison added.

- ◦Sale/Acquisition

- ◦Development