National CRE News In Your Inbox.

Sign up for Connect emails to stay informed with CRE stories that are 150 words or less.

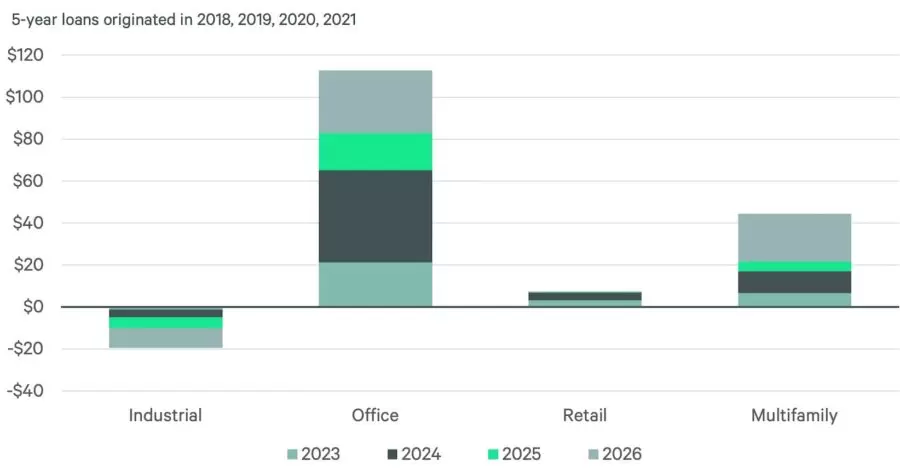

Report: Multifamily Sector and its Debt Funding Gap

In June 2023, CBRE reported “a substantial funding gap of $72.7 billion for office loans that would mature between this year and 2025.” At the time, funding gaps weren’t evident for the other property sectors. The company described funding gaps as investors being “forced to refinance at a loan-to-value (LTV) ratio lower than the one at which they first borrowed, or when the value has fallen since the loan was originated.”

But a recent report from CBRE Econometric Advisors shared that the office debt funding gap increased to $82.9 billion and that a $21.7 billion funding gap was evident for multifamily properties. The report explained that 2021 vintage loans were added to the analysis, further increasing the funding gap for loans coming due between now and 2026 to $112.8 billion for office and $44.54 billion for multifamily.

“’Vintage’ refers to the year of origination,” CBRE Senior Research Data Analyst Michael Leahy told Connect CRE. “In other words, they were commercial mortgages issued in the year 2021.” He said that many multifamily investors at the time used short-term floating-rate debt with extremely low interest rates to buy properties. “For some, this is catching up with them in a negative way,” Leahy added.

Maturities Don’t Equal Distress

There have been multiple negative headlines concerning CRE loan maturities, with the assumption that debt coming due involves a straight leap to distress, foreclosures and building “fire sales.” But this isn’t the case. Leahy indicated that loan maturities don’t automatically mean distress.

However, loan maturities in conjunction with value declines and less available credit is what creates the distress,” he said. “In these situations, owners are forced to put up more cash to keep their properties.” If owners are unable or unwilling to do this, defaults and distress can result.

The Other Sectors

Last summer, it was the office sector shouldering the debt funding gap. Now, in the fall, multifamily has been added to the mix. One logical question is whether the ranks of retail and industrial are likely to join this club. Leahy said no, at least not as of now.

“Industrial has had enough value gains in recent years to offset the decline in credit availability,” he explained. As for retail, the sector “had less debt originated than the other sectors between 2018-2021, with a smaller fraction of short-term debt,” Leahy commented.

- ◦Financing

- ◦Economy