National CRE News In Your Inbox.

Sign up for Connect emails to stay informed with CRE stories that are 150 words or less.

Report: Affordability Slows Single-Family Market

A combination of ongoing home price and mortgage rate increases is creating a huge affordability barrier in the single-family housing market. An analysis released by Zillow‘s Senior Economist Nichole Bachaud reported that home values are 24.7% above what is considered “normal” affordability. While buyers are feeling the brunt, sellers are impacted as well.

The Buyer Side

The analysis indicated that the share of household income on a mortgage for a typical home is “now significantly higher than it was in the nearly two decades preceding the pandemic,” Bachaud said. Breaking this down, the median household can now expect to spend 30.2% of income on principal and interest payments alone—not including taxes and insurance—when buying a home.

“A deep cut to home values or a significant bump to incomes are not likely to take place in the foreseeable future,” according to a press release detailing the analysis. As a result, “would-be buyers are going to be waiting a long time for the market to become affordable in the way it once was,” the release went on to say.

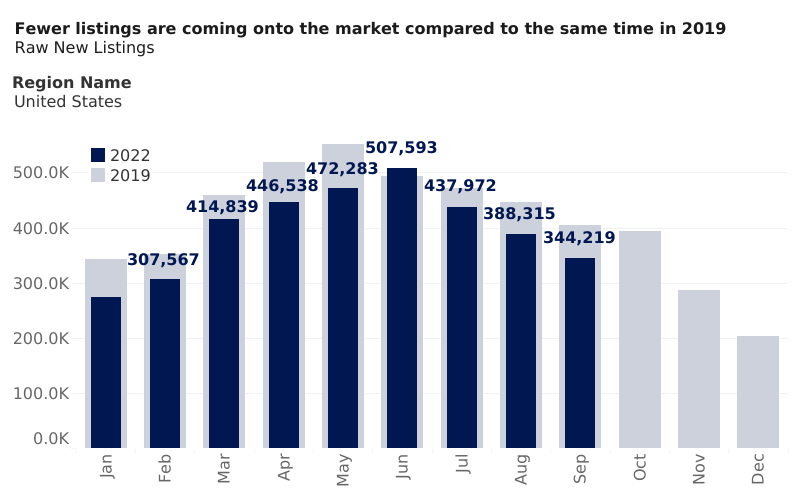

The Seller Side

Though the market favored sellers only a short time ago, would-be sellers “are hitting reset on their position within the market,” Bachaud said. One of the issues is that more than two-thirds of home sellers become home buyers. Because 90% of their mortgage rates are less than 6%, many would-be sellers believe they’re locked into those existing rates.

“This phenomenon of homeowners feeling locked in to their low mortgage rate is leading to a pullback in new listings hitting the market,” Bachaud noted. New listings in September 2022 were down 16% from the year before. Year to date, 11% fewer homes have been listed than during the same period in 2019.

Will Affordability Recover?

Bachaud notes that affordability isn’t likely to bounce back any time soon. Continued constrained inventory and pent-up demand drive home prices. Meanwhile, mortgage rates are approaching 7%. Additionally, while national income growth within the past year has been strong, so has core inflation.

As such, “while prices and mortgages rates are expected to stay high and incomes are not expected to meaningfully increase, the affordability outlook on mortgages is bleak,” Bachaud said.

- ◦Sale/Acquisition

- ◦Financing

- ◦Economy

- ◦Policy/Gov't