National CRE News In Your Inbox.

Sign up for Connect emails to stay informed with CRE stories that are 150 words or less.

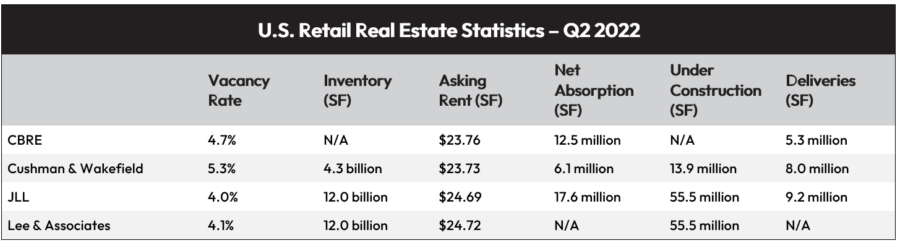

Q4 Retail Report: Ongoing Consumer Spending Drives Metrics

According to the U.S. Census Bureau, its just-released (preliminary) Advance Monthly Sales for Retail and Food Services totaled $700.3 billion in January 2024. This marked a year-over-year increase of 0.6%. The report also noted that sales between November 2023 through January 2024 were up 3.1% from the same period the year before.

That was for the first month of 2024. For the final quarter of 2023, consumer spending increases were one reason the CRE retail sector remained robust. Various Q4 2023 reports also cited ongoing tight space.

Specifically, “steady consumer spending and tenant demand pushed vacancy to record lows, making quality space for lease harder to come by,” according to Lee & Associates North America Market Review. Added JLL’s United States Retail Outlook: “Demand ramped up to finish the year strong, with the highest net absorption levels for 2023.”

Limited Construction

“New retail construction has been minimal since the pandemic and has retrenched further in light of higher interest rates and risk aversion by banks and other sources of financing,” Cushman & Wakefield’s Shopping Center MarketBeat Report explained. For the first time in years, the retail sector is becoming supply-constrained, “at least for space in quality shopping centers,” Cushman & Wakefield analysts added.

CBRE’s U.S. Retail Report agreed, pointing out that Q4 and annual construction completions hit lows “as construction costs remained prohibitive.” CBRE analysts also noted that community and strip centers were the hardest hit.

Despite this, Cushman & Wakefield analysts acknowledged that absorption is “slowing over a longer time horizon.” The analysts added that this isn’t necessarily due to a lack of demand but the lack of available quality retail space.

Sunbelt States Lead the Way

The reports were unanimous in noting that the Sunbelt markets were the most active in Q4 2023, with locations like Dallas and Charlotte, NC, experiencing an annual rent-growth increase of 5.4% and 5.8%, respectively, according to JLL metrics. “Leading the way in inventory-adjusted demand growth over the past year were Phoenix, San Antonio, Austin, Fort Lauderdale and Kansas City,” as retail continues to follow rooftop growth,” Lee & Associates analyst pointed out.

CBRE reported that Texas markets accounted for “five of the top 10 markets for 2023 annual net absorption” and approximately 25% of the 2023 national total. The Lone Star State also had the top three markets “and half of the top 10” for annual construction delivery, with Orlando and Miami rounding out the top five, the CBRE analysts added.

Cushman & Wakefield researchers also indicated that “the South accounted for more than half of the national absorption in 2023,” but overall demand had decreased 45% from 2023.

The Outlook

CBRE analysts predicted that ongoing costs and interest rates will continue to put a damper on new construction. JLL researchers agreed, pointing out that retailers will continue to be challenged to find desirable space.

Though the JLL analysts are forecasting new space deliveries to total over 63 million square feet, “much of that is preleased and consists of freestanding build-to-suit retail.”

Furthermore, any threat from new supply “is expected to remain minimal,” the Lee & Associates analysts commented. This state of affairs will likely exist “until new development pencils through a combination of moderating input costs and rising rents,” the analysts added.

Cushman & Wakefield predicted a moderation in retail fundamentals in 2024, along with leasing demand challenged due to limited space availability. As a result, “it’s difficult to envision vacancy rates going much lower, even in a robust economy,” Cushman & Wakefield analysts noted.

- ◦Lease

- ◦Economy