National CRE News In Your Inbox.

Sign up for Connect emails to stay informed with CRE stories that are 150 words or less.

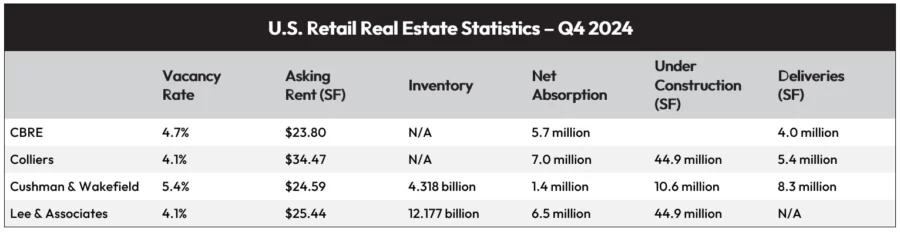

Q4 Retail: Continued Lack of Space Despite Bankruptcies and Closures

From retailers’ perspectives, the holiday season was robust. However, retail in Q4 2024 was also characterized by bankruptcies and store closures. Despite this, reports cited low absorption and sub-5% vacancy rates, primarily due to a lack of useable space. Colliers U.S. Retail Market Statistics stated that “tenants and brokers cited a lack of quality space as a key market challenge.”

Absorption Issues

Three of the four reports studied indicated sluggish absorption, primarily due to the above-mentioned lack of space. Lee & Associates’ Q4 2024 North American Market Report said that tenants looking for “high-quality space in affluent areas aren’t finding many options. CBRE’s U.S. Retail report agreed, adding that 25 of the 69 markets the company tracks reported negative net absorption, “contributing to the lowest annual total demand since 2020.”

Meanwhile, Colliers’ analysts noted that store closures also impacted absorption but added that the new space provided “much-needed supply for those tenants looking to expand.”

Furthermore, Cushman & Wakefield’s Retail MarketBeat was more optimistic about absorption, pointing out that Q4 “registered the strongest net absorption of 2024,” indicating that “the retail market is in a healthy spot heading into 2025.”

On the Construction Front

All reports agreed that the lack of new space was a prime reason for subdued absorption. Colliers analysts noted that new development is at a “multi-decade low,” while CBRE analysts added that “developers have shelved projects, exacerbating the retail supply shortage.”

One reason for the shrinking pipeline is the high materials and labor costs. Another cause is tightening lending standards. As such, “developers continue to be challenged to make ground-up retail development deals pencil at today’s costs and rent levels,” according to Lee & Associates’ analysts.

Looking at 2025

Consumer confidence is expected to remain strong, but the impact of tariffs remains a question mark, especially for consumer-facing industries, according to Cushman & Wakefield analysts. Despite this, “high-performing brands are likely to go forward with store openings in 2025,” they added.

However, despite more anticipated store closures, the lack of space could remain a problem. Colliers analysts anticipate that construction constraints will continue over the next year, while Cushman & Wakefield experts pointed to limitations on market expansion that will likely remain in place.

The analysts with Lee & Associates predicted that this year’s environment will likely support additional landlord rent gains while allowing “supply-constrained conditions to persist for the foreseeable future.”

- ◦Lease

- ◦Economy