National CRE News In Your Inbox.

Sign up for Connect emails to stay informed with CRE stories that are 150 words or less.

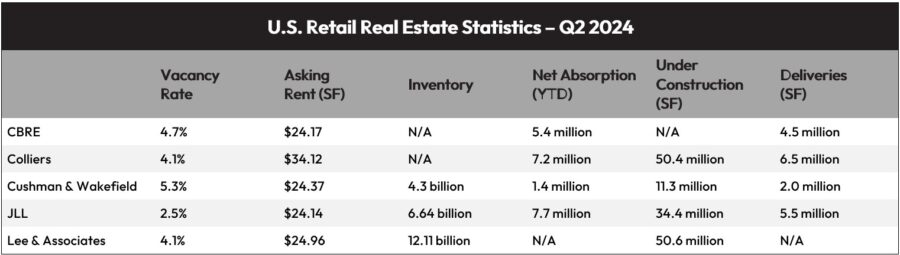

Q2 Retail: Ongoing Supply Limitations Mute Absorption Rates

The content from Q2 commercial real estate retail reports wasn’t much different from that of Q1 reports. Specifically, limited construction starts and deliveries have meant continued low vacancy rates and muted absorption.

More Space Taken, But . . .

Speaking of which, absorption did increase quarter over quarter, primarily “due to a reduction in move-outs and space taken in community centers, lifestyle centers and Class C malls,” noted JLL’s United States Retail Market Dynamics report.

Still, absorption rates in Q2 significantly undercut those reported in Q1 due to limited supply. Cushman & Wakefield’s U.S. National MarketBeat Shopping Center Q2 2024 report stated, “Absorption is on track for a lackluster year.” Overall, the national vacancy rate remained steady in Q2, “driven by rising demand, fewer tenant bankruptcies and limited new supply,” according to Colliers U.S. Retail Market Statistics 24Q2 report.

Lee & Associates’ Q2 2024 Market Report (retail) explained that recent growth in leasing and absorption was driven by food-and-beverage, discount, health and beauty, off-price and experiential retailers. “Most of the focus is spaces of 2,500 square feet or less and overwhelmingly is driven by growth from quick-service restaurants,” the Lee & Associates analysts commented.

The above-mentioned trend has led to a landlord-dominated market; JLL analysts commented that landlords have greater pricing power and are more selective regarding tenant choices.

The Outlook: More of the Same

The outlook doesn’t demonstrate much change, especially as higher construction costs mean less is being built. CBRE’s Q2 2024 U.S. Retail Figures explained that costs for new retail development range between $400 and $500 per square foot, and “few markets command average rent that is high enough to justify such an expense.”

Cushman & Wakefield analysts commented that the lack of space will put downward pressure on retailer expansion plans. On the other hand, retail bankruptcies and mergers could also drive more store closures. Those closures – especially of retail pharmacies (think Walgreens) and dollar stores – could open more space for freestanding retail operators, JLL analysts pointed out.

JLL analysts also forecast a stabilization of capital market transactions in 2H 2024, which could lead to an increase in investments.