National CRE News In Your Inbox.

Sign up for Connect emails to stay informed with CRE stories that are 150 words or less.

Preview: 2023 U.S. Mid-Year Economic Update from Berkadia

Market expectations of rate hikes or cuts for the remainder of the year have been significantly reshaped over the month of May and early June. While the Federal Reserve hiked rates by 25 basis points at their May 3rd meeting, all the fireworks came with the mid-June meeting, as the newly released Summary of Economic Projections indicated much of the Fed favored at least another 50 basis points of rate hikes this year.

The market’s repricing of the Fed’s rate hikes and cuts over the month of May can be visualized through Bloomberg’s World Interest Rate Probability (WIRP) function. The WIRP function portrays the market’s perceived probability of a Fed hike or cut at upcoming meetings. Following the May 3rd Fed meeting, the market expected that the Fed would begin cutting rates later in 2023.

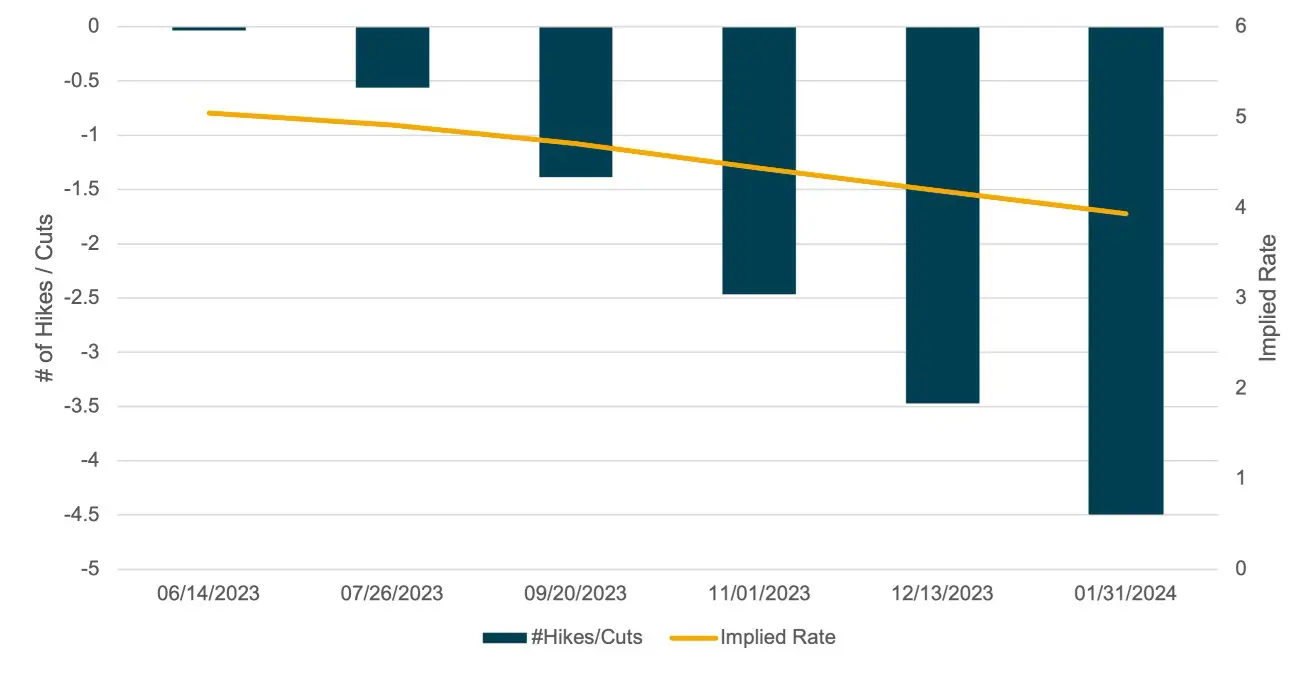

Fed Funds Interest Rate Path as of May 4, 2023

Source: Bloomberg LP

On May 4th, the market expected:

- No rate hike in June

- A cut as early as September

The possibility of additional future rate hikes increased dramatically over the subsequent weeks due to the released economic prints, including the monthly Consumer Price Index (CPI), monthly Personal Consumption Expenditures price index (PCE), and finally the nonfarm payrolls print. The year-over-year Core CPI print held relatively steady on both a month-over-month and year-over-year basis, reinforcing inflation is sticky and will take time to get back to the Fed’s two percent year-over-year goal.

Finally, the nonfarm payrolls print of 339,000 versus the expected 195,000 combined with upward revisions of the previous two months by 93,000 was significantly above trend. When adding those three prints to average hourly earnings holding roughly steady at 4.3 percent, it tracks that the market was repricing future hike expectations.

Following these economic prints, Fed speak regarding upcoming FOMC decisions guided the market towards the possibility of a pause in June and hike in July. This pause would give Fed officials more time to assess the effects of past rate increases, and this Fed speak not only shifted expectations for a 25-basis-point hike in July instead of June, but it also transformed the expectations for Fed meetings in late 2023 and early 2024.

On May 4th, the market was expecting multiple rate cuts before the end of 2023. The market now expects the Fed to hold rates higher for longer than previously thought, pushing back the probability of cuts in 2023.

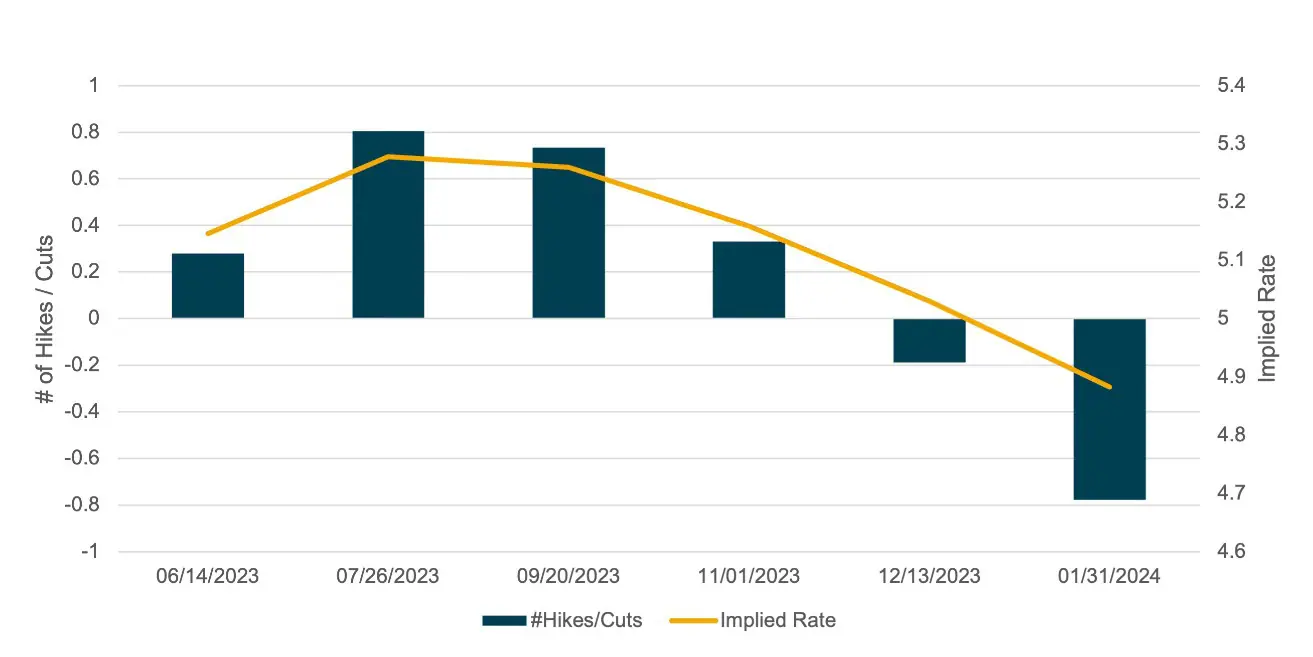

Fed Funds Interest Rate Path as of June 9, 2023

Source: Bloomberg LP

On June 9th, the market expected:

- A higher likelihood that a rate hike would come in July, instead of June

- Higher likelihood of a rate cut in early 2024

The June meeting provided a unanimous vote amongst committee members to hold its benchmark rate in the 5.00 to 5.25 percent target range, but the press conference and forward projections were the real meat. The FOMC statement gives a clear signal that policymakers will resume tightening and the median forecast of the Fed’s updated dot plot calls for an additional two rate hikes in 2023. According to WIRP, the market is pricing in a 25-basis-point hike in July, with a possibility of another hike in September.

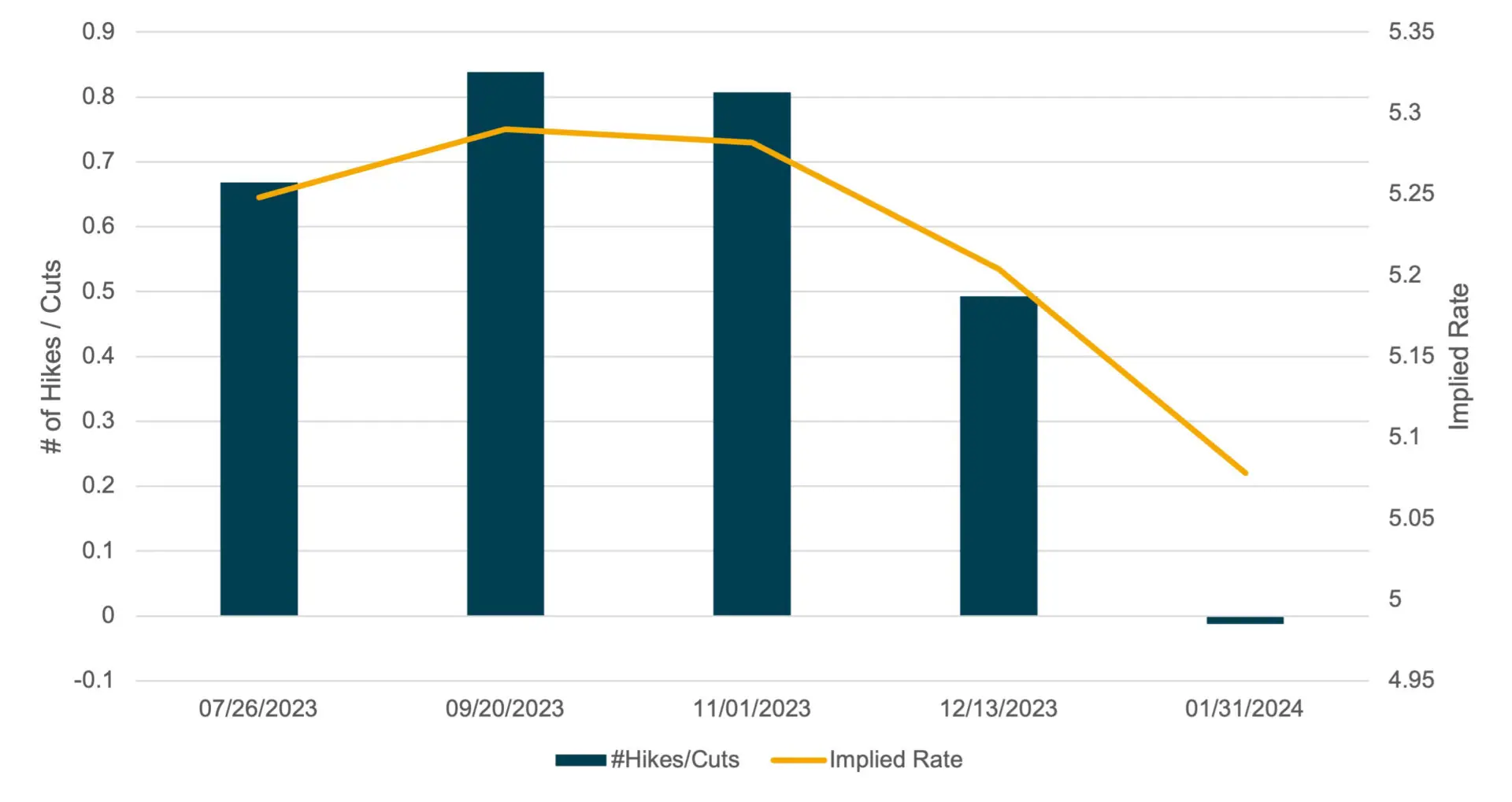

Fed Funds Interest Rate Path as of June 15, 2023

Source: Bloomberg LP

On June 15th, the market expects:

- A high possibility of a hike in July, with a slight chance of an additional hike in September

- The possibility of a rate cut is not above 50 percent until January 2024

While the statements, Fed speak, and projections provided by the Fed after meetings have moved market expectations of hikes and cuts, it has only done so over the short-term horizon. Even now, when the Fed Chair is saying rate cuts could be a ‘couple years out’, the market is pricing in reductions by January of next year. It seems the market needs to be reminded that one of the best-known investment edicts is “don’t fight the Fed”.

Want more insights?

Join Berkadia’s upcoming Beyond Insights Webinar: 2023 U.S. Economic Update, featuring guest speaker Randy Quarles, Former Vice Chairman of the Federal Reserve System, on Thursday, June 22. Mr. Quarles will offer his perspective into the current economic climate and its anticipated impact on commercial real estate.

Can’t join? Register anyway to receive a copy of the recording.

- ◦Financing

- ◦Economy