National CRE News In Your Inbox.

Sign up for Connect emails to stay informed with CRE stories that are 150 words or less.

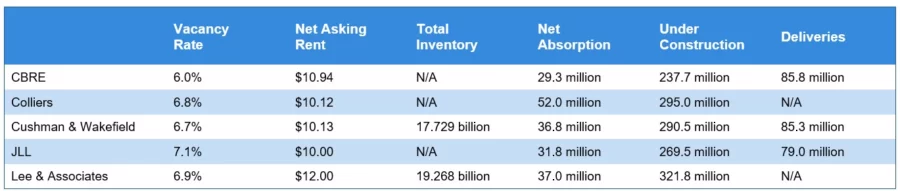

Industrial: Sector Poised for Growth

The industrial construction boom took place between late 2020 and 2022. Demand for warehouse and logistics space drove speculative builds. However, construction—and absorption—fell from 2023 onward as demand waned due to higher interest rates and geopolitical factors. According to Q4 2024 reports, we’re close to the bottom of that drop, if not already there.

Still, “despite headwinds throughout the year—including high interest rates, inflation, labor disputes and election uncertainties—the U.S. industrial market remained resilient, with modest growth persisting,” said Cushman & Wakefield’s MarketBeat Industrial Report.

On the other hand, “the industrial sector finished 2024 with tenants continuing to exercise prudence by postponing significant commitments amid persistent ambiguities in the market,” according to JLL’s United States Industrial Market Dynamics.

Ongoing Brakes on Absorption, Construction

CBRE’s U.S. Industrial Report pointed out that annual absorption slumped to its lowest level in years. Construction completions also dropped precipitously. Additionally, “both asking and taking rents declined for the third consecutive quarter, as landlords focused on occupancy,” the CBRE analysts said.

Meanwhile, Colliers’ U.S. Industrial Market Statistics Report noted that “the U.S. industrial vacancy rate is nearing its peak as construction activity normalizes to pre-pandemic levels and demand gradually recovers.”

JLL analysts indicated that economic uncertainties, ongoing deliveries, a move to smaller lease sizes and a reduction in speculative deliveries contributed to the absorption and construction metrics. Cushman & Wakefield analysts agreed, adding that high interest rates, inflation, labor disputes and election uncertainties played a role in sluggish absorption, construction and asking rents. Tenants also consolidated efforts to reduce their costs while improving efficiencies.

Lee & Associates’ Q4 2024 Market Report also explained that business owners had paused their expansion plans as far back as 2023, and “caution continued to hobble growth plans in 2024, pending the general election and its effect on tariffs.”

Outlook—Industrial to Achieve Balance

According to JLL analysts, the sector is approaching the bottom of the current cycle and is “poised for growth.” Vacancies are anticipated to increase marginally in the first half of 2025, though in higher-vacancy markets, more concessions could be the norm. At the same time, rents “are expected to stabilize in 2025 as the markets reset,” Colliers analysts said.

CBRE analysts anticipated that “a decline in starts will lead to significantly less first-generation space on the market in coming quarters.” JLL analysts noted that this could be coupled with demand from logistics companies due to a growth in nearshoring strategies.

Lee & Associates analysts indicated that an even marginally positive net absorption could slow the upward trend of vacancy rates in 2025. “The continued reduction in industrial construction starts that occurred in late 2024 also raises the probability that the U.S. vacancy rate could begin to decline by late 2025 or early 2026,” they added.

Additionally, new supply reduction “is expected to help achieve balance more quickly than if high levels of construction had persisted,” observed the Colliers analysts. Cushman & Wakefield analysts shared the optimism, pointing out that despite the potential headwinds caused by possible tariffs and geopolitical risks, “the U.S. Industrial market is poised for growth in 2025.” With the decrease in deliveries and fewer construction starts, “vacancy rates should stabilize, likely peaking in the first half of the year before slipping downward,” they added.

However, the metrics will greatly depend on the market. “Certain markets continue to build more product than others, which will drive vacancy rates higher in those areas and result in a longer recovery period,” the Colliers analysts pointed out.

Additionally, though “new deliveries have peaked, several Sunbelt and Midwest markets with fewer constraints on new development are still in the midst of a record supply wave that could take tenants more than two years to fully absorb,” added the Lee & Associates analysts.

Register Today to “Be in the Room” when Michael Brennan receives Connect CRE’s Lifetime Achievement Award and will participate in the Keynote Interview with Kevin Brennan, also of Brennan Investment Group. Join us at Connect Industrial Midwest 2025 on the afternoon of Wednesday, March 5, at Joe’s Live in Rosemont, IL, for this exclusive presentation!

- ◦Lease