National CRE News In Your Inbox.

Sign up for Connect emails to stay informed with CRE stories that are 150 words or less.

Hospitality – Another CRE Sector Facing Debt Maturities

Commercial real estate debt maturities have been in the news for over a year. But most stories focus on maturing loans for office and multifamily properties. A recent JLL report shed some light on another sector for concern – hospitality. Specifically, $5.8 billion of U.S. hotel single-asset securitized loans (like CMBS and CRE CLOs) are coming due in 2024. While the hotel industry has enjoyed great RevPAR numbers, “there are multiple headwinds that could impede the refinancing of these securitized loans and compel owners to transact instead,” the JLL report said.

Lagging Profitability

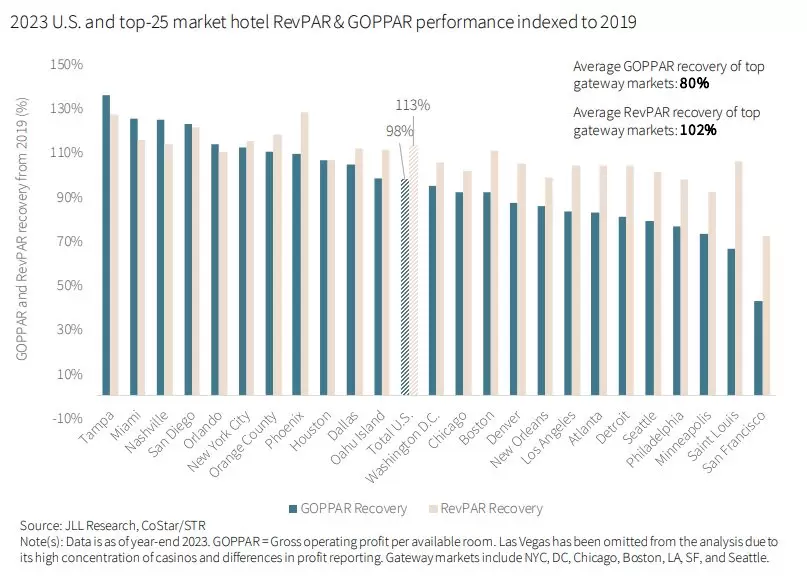

One of those headwinds is profitability. Certainly, 2023 RevPAR levels exceeded those in 2019 by 13.2% due to increased leisure demand and a return of business and group travel. “Despite this . . . profitability has remained elusive in markets heavily reliant on the recovery of international business and group demand,” the report explained.

These markets also continue to struggle with other issues, such as increases in labor costs, property taxes and operational expenses. The report said the impact of these headwinds is especially prevalent in gateway markets.

Persistently High Interest Rates

Then there are the higher-for-longer interest rates. Like other commercial real estate sector investors, hospitality owners face the issue of refinancing at higher interest rates. And those rates have exploded; JLL experts indicated that since 2020, the average fixed interest rates for U.S. hotel securitized loans increased by 332 basis points, reaching 7.7% in Q1 2024. Nor are floating rates doing much better at an average of 8.3%.

As indicated by the recent Federal Open Market Committee Meeting, the Federal Reserve isn’t in any hurry to start cutting its Effective Federal Funds Rate (EFFR). “Consequently, borrowers facing impending loan maturities will find refinancing to be an unfavorable option” and will consider selling the property, the JLL analysts said.

Increasing Property Insurance

Another metric that continues increasing is property insurance costs. Much of this is due to inflation and growing weather hazards related to climate change. Regardless of the reason, increased costs are creating “a significant challenge to hotels, disrupting their cash flows and elevating their credit risk,” the JLL analysts wrote in the report. Those at the most risk are properties in coastal gateway markets.

Cash flow disruption is problematic as it becomes more challenging to meet debt service obligations.

What it Means

The report’s authors suggest that if the $5.8 billion due were to be refinanced at current interest rates, “a large majority of them would struggle to generate enough income to cover their debt costs.” On the other hand, JLL forecasts that the number of maturing loans in critical stress (totaling $4.2 billion in 2024) will decline over the next few years. As such, “this presents a short, near-term window of opportunity for investors to take advantage of the market dislocation,” the JLL analysts commented.

- ◦Sale/Acquisition

- ◦Financing

- ◦Economy