National CRE News In Your Inbox.

Sign up for Connect emails to stay informed with CRE stories that are 150 words or less.

Examining Grocery Chain Opportunities in Underserved Markets

Grocery stores, superstores and dollar stores share one thing. They carry food products. According to Placer.ai, grocery stores go a couple of steps further, offering consumers a variety of fresh foods. However, in a recent white paper, “Unlocking Potential in Underserved Grocery Markets,” Placer.ai analysts suggest that areas supporting a “robust dollar store presence” also suffer from a lack of grocery stores.

Coast versus Interior

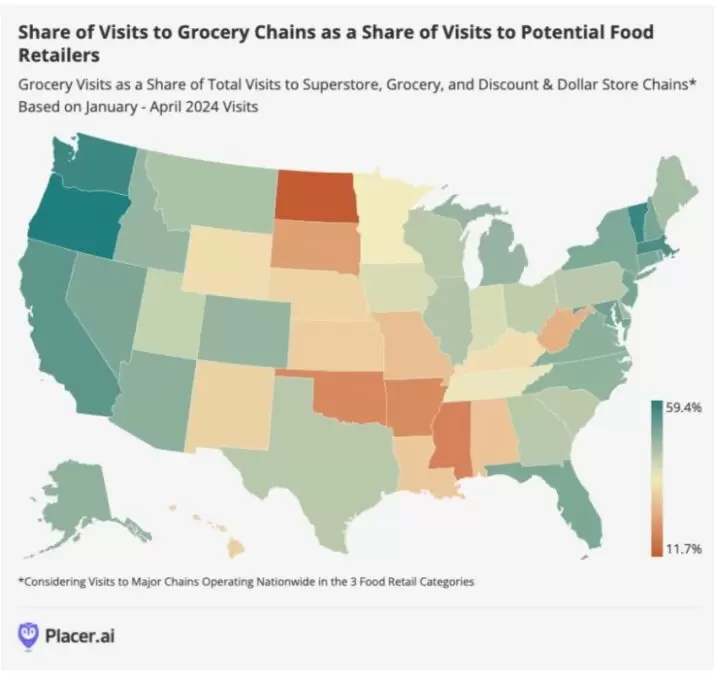

The white paper indicated that the ten states where residents were more likely to visit grocery chains in early 2024 were on the East and West Coasts, including Oregon, Vermont, Washington State, Massachusetts, California, Maryland, New Hampshire, Connecticut, New Jersey, and Rhode Island. These accounted for 50% or more of food retail visits between them.

But the story differs in the West North Central and South Central states. In North Dakota, grocery chain visits accounted for 11.7% of food retail visits. The white paper said that grocery stores in Mississippi, Oklahoma and Arkansas attracted less than 20% of overall food retail traffic.

No Lack of Interest

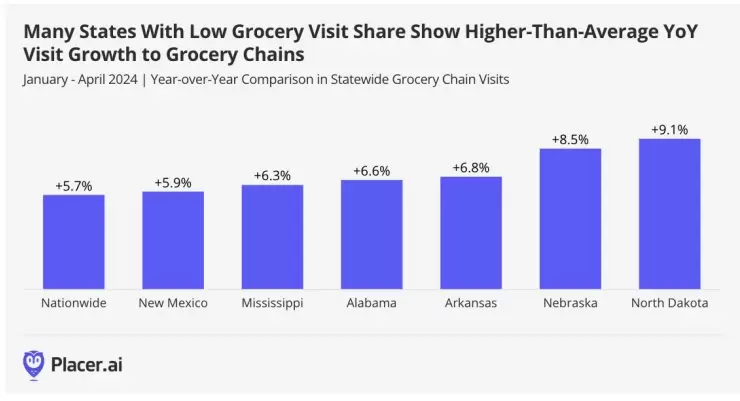

The white paper explained that the low grocery store visit share in some of the states analyzed doesn’t mean an inability to support the stores or a lack of consumer interest. “In some of these underserved regions, existing grocery chains are seeing outsize visit growth, indicating growing demand for their offerings,” the white paper pointed out.

For example, North Dakota clocked a 9.1% year-over-year increase in grocery visits between January 2024 and April 2024, nearly double the national average of 5.4%. Other states with lower grocery visit shares also experienced higher-than-average YoY grocery visits. “This suggests significant untapped potential for grocery stores and a market that is hungry for more,” the white paper said.

The white paper also focused on Alabama, where grocery chains account for a smaller share of overall food retail traffic (28.9%), while YoY visit growth (6.6%) outperformed the national average. The white paper explained that the low visit share could be due to inadequate supply rather than lack of demand. For example, in Central Alabama, “many residents drive at least 10 miles to reach a local grocery store chain,” the white paper said. Meanwhile, several parts of the state (rural and urban) offer “clusters of grocery stores that draw customers from relatively far away.”

Reconsidering Grocery Store Locales

The white paper suggested that the issue for grocery stores in underserved areas isn’t a lack of interest but rather a lack of accessibility. This doesn’t necessarily mean high-end grocers – think Trader Joe’s or Sprouts – would be ideal for such locations. The white paper indicated that consumers of Greenville County (South Carolina) would likely be interested in “Mid-Range Grocery Stores,” which encompasses brands including Aldi, Kroger and Lidl. “This metric provides further evidence of local demand for grocery chains and offers a glimpse into the kinds of grocery offerings likely to succeed in the area,” the white paper explained.

The white paper suggested that underserved grocery markets could be a good opportunity for expanding grocery chain operators. The same goes for civic leaders who want to increase healthy food options in their communities. “For both groups, identifying underserved markets with significant untapped demand can be a critical first step in deciding where to focus grocery development initiatives,” the white paper said.

- ◦Development

- ◦Economy