National CRE News In Your Inbox.

Sign up for Connect emails to stay informed with CRE stories that are 150 words or less.

Beyond the Maturity Wall: Why Multifamily’s Next Refinance Cycle Looks More Workable Than the Headlines Suggest

By Tina Quirin, Principal, Arcus Harbor Real Estate Capital

The multifamily maturity wall has been a looming concern for several years. Through the rest of 2026 and into 2027, borrowers will be working through loans that were originated in a very different rate environment; often with leverage, pricing, and underwriting assumptions that today’s market will not fully support. At the same time, the financing landscape has become materially more open, competitive and flexible than it was a year ago.

Capital solutions now are more varied than when rates first moved higher, although many now require greater structure and additional sponsor equity than in prior cycles. For sponsors who engage early, the current environment presents an opportunity to recapitalize proactively rather than reactively.

The Story Behind the Numbers

The size of the maturity wall tells only part of the story. Equally important is its composition.

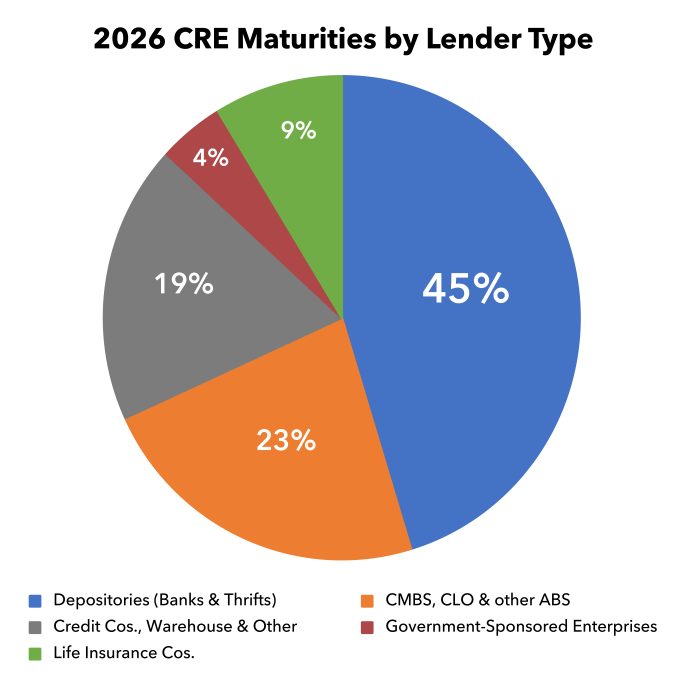

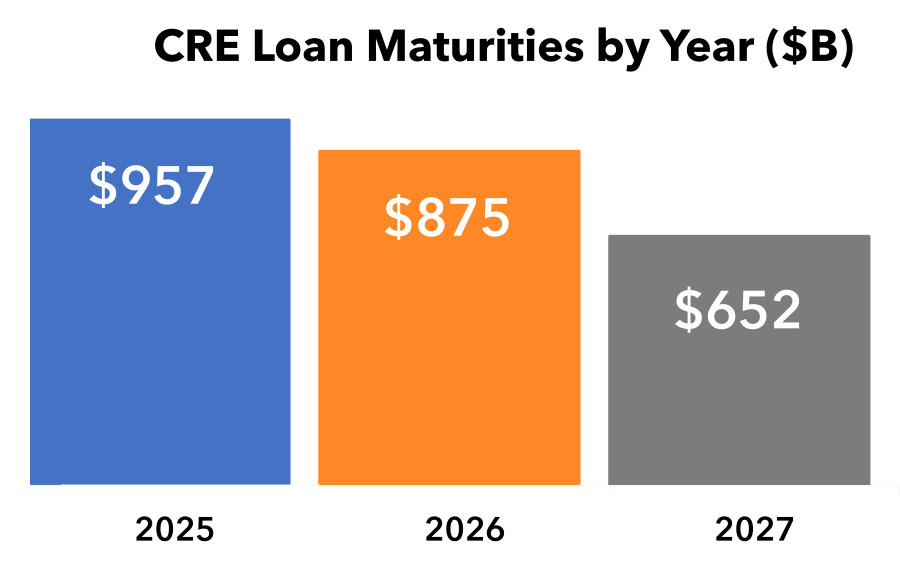

The Mortgage Bankers Association estimates that $875 billion of the $5 trillion in outstanding CRE loans is due to mature in 2026, followed by another $652 billion in 2027. But these maturities are far from evenly distributed across asset and lender types. Depositories, CMBS/CLO/ABS lenders, credit companies, and warehouse lenders account for roughly 75% of 2026 CRE maturities. Agency maturities are more heavily concentrated in the later years of the cycle, with the peak hitting in 2029-2030.

Within multifamily specifically, banks hold 24% of debt maturing between 2025 and 2033, with 43% of those maturities coming due through 2027. Debt fund maturities show a similar front-loading, with 21% of their maturities concentrated in the near term compared with 18% for the overall market.

The takeaway is that current refinancing stress is not evenly distributed across the multifamily market, and the issue is often less about asset viability and more about whether the existing capital stack still aligns with current lending standards.

Capital is Available, but Disciplined

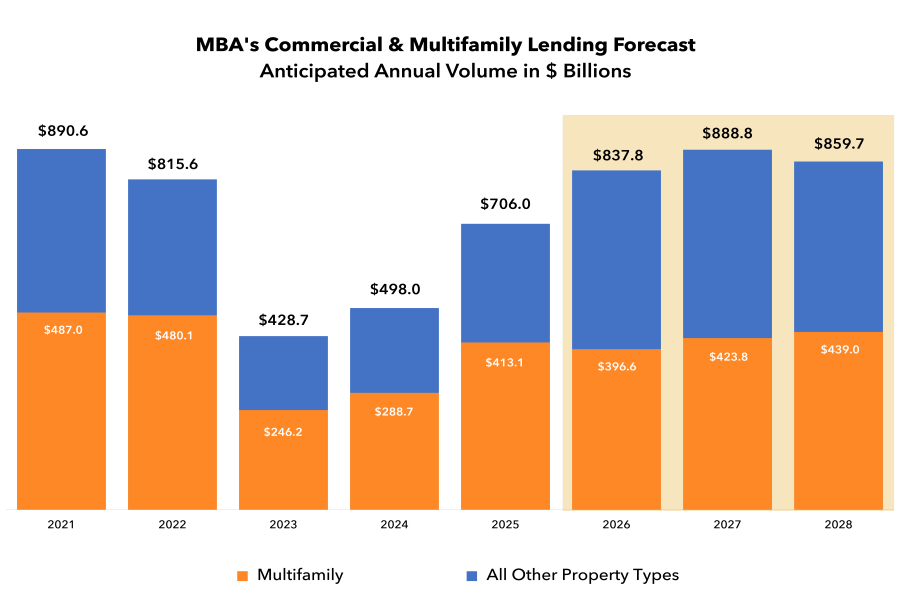

The refinancing environment is materially better than it was a year ago, even if it remains highly selective. As of midyear, MBA forecasts commercial mortgage origination volume will rise from $706 billion in 2025 to $838 billion in 2026, followed by $888 billion in 2027. Multifamily is expected to account for nearly half of those totals each year.

Still, tighter spreads have not translated into lower all-in borrowing costs. Treasury and SOFR rates remain elevated relative to the prior cycle, leaving many borrowers refinancing into materially higher rates than their existing debt. Even so, lenders are increasingly willing to transact where sponsorship, leverage and asset performance support the deal.

Solving With Structure

Perhaps the most significant shift in this cycle is the expanding use of structured capital solutions. Borrowers refinancing today are confronting benchmark rates that remain materially above the weighted-average interest rates on their maturing loans. For many borrowers, the question has shifted from who will lend to what capital structure makes the most sense for the asset’s next phase and the next maturity beyond it.

While the agencies remain central to multifamily refinancing, particularly stabilized assets, they are no longer the automatic solution for every maturity. Banks have become more active relative to the past two years, and debt funds continue filling the gaps for assets undergoing stabilization or repositioning or situations requiring higher leverage, shorter duration, or flexibility. Preferred equity has also become increasingly common where senior loan proceeds alone cannot bridge refinance gaps.

Lender behavior has also evolved. The extend-and-pretend period of 2023-2024 reflected a belief that lower rates or stronger operating performance would eventually resolve refinance challenges. Today, lenders are drawing sharper distinctions between assets where fundamentals improved and situations where extensions merely delayed the need for recapitalization.

In response, borrowers are increasingly turning to rate buydowns, lower-leverage structures, preferred equity, and shorter-duration bridge executions to preserve flexibility. In today’s market, execution and creative structuring often mean the difference between successfully resolving a maturity or moving into a modification or extension, likely with some level of paydown, that buys time without addressing the capital stack issues.

Distress Remains Contained

The obvious question is whether these refinancing challenges ultimately translate into broader market distress.

Distress in the multifamily market is real, but it remains concentrated rather than systemic. Pressure is concentrated in assets with higher leverage, weaker debt yields, transitional business plans, and/or softer operating performance. CMBS delinquency and special servicing rates have risen, driven largely by operational challenges, weaker loan structures and stress concentrated in select markets and non-agency lending channels. Agency-backed multifamily debt, by contrast, continues to demonstrate relatively healthy performance metrics.

While some assets will still require fresh equity, the combination of available capital, improving lender participation and broader structural solutions points to a market that appears more capable of resolving upcoming maturities than headlines often suggest. For many borrowers, the challenge today is less about access to capital and more about timing, structure, and proactive execution.

The Takeaway:

The maturity wall is real, but it’s comprised of a mixed bag of debt. Some loans will refinance smoothly, others will need a bit of creative recapitalization, and a portion of assets will face more difficult restructurings.

Still, the good news is that the market is in a better place to handle it today than it was even a year ago. More lenders are active, the range of available capital solutions has expanded, and refinancing outcomes are increasingly being decided deal by deal rather than constrained by a single market narrative.

For sponsors willing to engage early and thoughtfully explore the full toolkit of available structures, many fundamentally sound deals remain financeable. Rather than broad-based collapse, this cycle increasingly resembles a prolonged resolution process in which preparation, structure, and execution will make all the difference.

- ◦Financing