National CRE News In Your Inbox.

Sign up for Connect emails to stay informed with CRE stories that are 150 words or less.

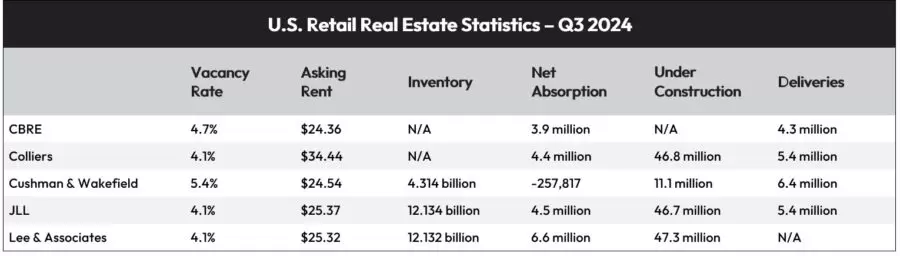

Low Absorption, Less Space Highlight Retail Space in Q3

Reports discussing the U.S. retail market in Q3 2024 reiterated the same theme. Namely, flat or declining absorption, little new construction and higher asking rents. Or, as Lee & Associates’ Q3 2024 Retail Overview said, “U.S. retail real estate heads into the second half of 2024 in one of its tightest fundamental positions on record, thanks to steadily rising demand, a reduction in tenant bankruptcies and store closures, and limited new supply.”

On the absorption front, Lee & Associates put the number at 6.6 million. Meanwhile, Cushman & Wakefield’s Q3 2024 Shopping Center Report had absorption in negative territory, at -257,817 on the quarter, though it allowed that some of the reason for the weakness was the aftermath of Hurricane Helene.

All the reports pointed to subdued construction starts and deliveries. “Construction starts have declined over the past two years due to rising costs, resulting in historically low levels of new retail development across the U.S.,” said Colliers U.S. Retail Market Statistics 24Q3 analysis.

The lack of space and ongoing tenant demand drove rents upward, according to CBRE US Retail Figures Q3 2024 report. “Rising construction and borrowing costs have significantly curtailed new development,” the CBRE analysts added.

With little space coming online, JLL’s United States Retail Outlook Q3 2024 report pointed out that competition is fierce regarding quality locations. Cushman & Wakefield analysts agreed that “prospective tenants will remain challenged with finding available space, particularly in high-quality shopping centers in the most sought-after markets.”

Nor is the situation likely to change in the near-to-mid period. The JLL report forecasts an upbeat holiday season, with shoppers planning to spend more money this year and almost twice as many of those shoppers planning to use curbside pickup.

Moving into 2025, Cushman & Wakefield analysts point out that new retail space will come online in small batches, meaning “prospective tenants are likely to have limited options in the most sought-after locations.”

Meanwhile, as closures spurred by Walgreens, CVS, Big Lots, and others continue, the JLL analysts added that this could create more opportunities for tenant backfill and expansion. Cushman & Wakefield agreed that more store closures than openings could help with cautious real estate expansion plans.

- ◦Lease

- ◦Development

- ◦Economy