National CRE News In Your Inbox.

Sign up for Connect emails to stay informed with CRE stories that are 150 words or less.

Should There Be a Concern About Elevated Consumer Debt?

It’s a truism that spending and consumption drive the U.S. economy. If that spending and consumption are threatened in any way—like, for example, if consumers are borrowing too much—this could be a problem.

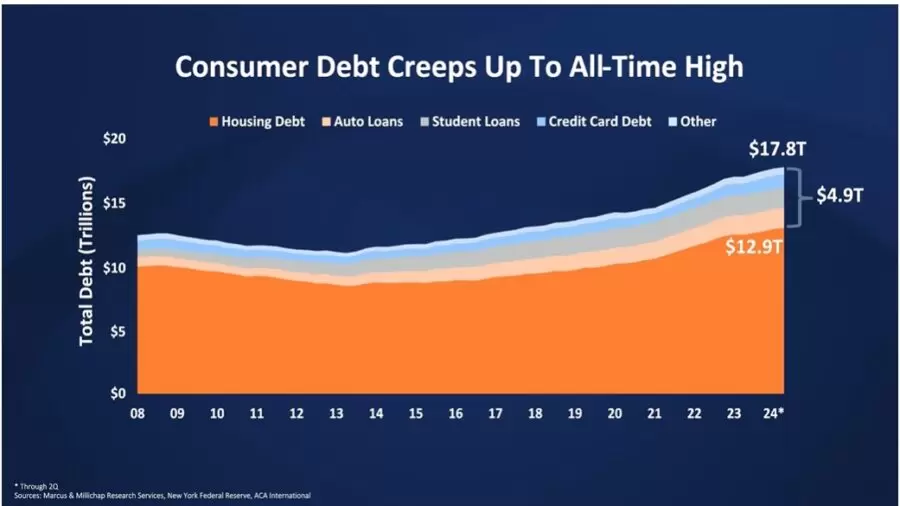

On the surface, there is that problem. The Federal Reserve of New York’s Q2 2024 Household Debt and Credit Report said household debt stood at $17.8 trillion. This number, in turn, generated numerous headlines about the increase.

John Chang, Marcus & Millichap’s Senior Vice President, National Director, Research and Advisory Services, acknowledged the high debt. In a video, “Will Elevated Debt Threaten the Economy?” He broke down the debt:

- $12.9 trillion consists of mortgages and home equity lines of credit

- $1.6 trillion consists of student loans

- $1.6 trillion consists of auto loans

- $1.3 trillion consists of credit card debt, which is at a record high

“All of this sounds like dire news,” Chang said. “But there are two sides to the story.”

First, job growth continues. There are 7.7 million more jobs than in 2019, before the pandemic. Second, wage gains are expanding more quickly than inflation.

What about household debt service payments as a percentage of disposable income? Chang acknowledged that the 11.5% is at its highest level since the pandemic. But the pandemic skewed economic results, between lack of spending due to the lockdown and consumer receipt of stimulus checks.

Instead, Chang went back to the period between 2014-2019, which he called the “normal times following the recovery from the global financial crisis but before the onset of the pandemic.” In that period, the average household debt service payment as a percentage of disposable income was 11.7%. In other words, slightly above where we are now.

This isn’t to suggest that consumer debt is a problem. “I think there’s a bit of a bifurcation here,” Chang said. “The lowest-income households do face disproportionate debt and economic headwinds that are showing up in elevated credit card consumer finance and auto loan delinquency rates.”

Yet even here, the delinquency rates are below where they were during the GFC. “While some households face substantial economic pressure, most people are in a relatively strong financial position,” Chang said. “As a result, consumption will likely remain healthy.”

Here’s how Chang broke down the CRE impact:

- Consumption will improve retail space demand and industrial demand as a byproduct

- Job and wage growth should bolster demand for rental housing and self-storage space

- Strong household balance sheets tend to support leisure travel, which could improve hospitality numbers

- ◦Economy

- ◦Policy/Gov't