National CRE News In Your Inbox.

Sign up for Connect emails to stay informed with CRE stories that are 150 words or less.

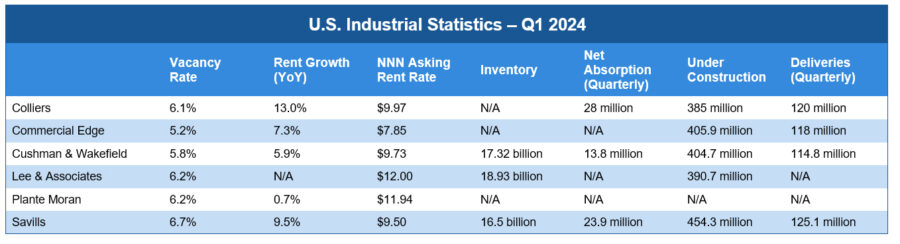

Industrial Q1: New Supply Continues to Push Vacancy Rates as Pipeline Shrinks

From about the middle of 2022, the industrial sector was marked by record-high demand, leading to record-low vacancy rates and accelerating rent growth. Numbers from Q1 2024 industrial reports show that the pendulum is swinging in the other direction.

“New industrial supply continued to push vacancy rates higher in all four regions of the country during the first quarter of 2024,” according to Colliers’ US. Industrial Market Statistics report. However, all indications are that the supply will soon slow. Savills’ State of the U.S. Industrial Market report said construction hit a low point during the first quarter. The CommercialEdge National Industrial Report agreed with this assessment, noting that the pipeline is “roughly two-thirds the size of last year’s volume.”

On the other side of the coin, demand is dwindling, as evidenced by decreasing absorption rates. “Interest rate hikes by central banks aiming to tame inflation and tenants battling supply chain and other issues continue to slow industrial demand across the United States and Canada,” the Lee & Associates North America Market Report pointed out. CommercialEdge analysts also commented that the e-commerce boom that had fueled much of the demand has cooled, even as “tenants have been much more hesitant to sign leases in the face of economic uncertainties driven by high inflation and interest rate increases.”

While the decrease in demand was expected, Cushman & Wakefield’s U.S. National MarketBeat Industrial Report acknowledged surprise at its extent, adding that it’s something “we will be keeping a close eye on.”

Regarding the outlook, Cushman & Wakefield analysts noted that touring activity has increased in recent months, “which should help keep leasing activity healthy and above pre-pandemic averages.” Savills analysts also commented that supply is edging closer to balance, “signaling turnaround on the horizon.”

Meanwhile, rent increases will likely continue for the remainder of 2024. “They will be more in line with historical average increases, while rental rates will contract in markets where rent increases got a bit out of hand,” Colliers analysts commented.

A shrinking pipeline is anticipated to impact vacancy rates beginning in 2025. However, Savills and CommercialEdge analysts sounded a couple of cautionary notes. Savills pointed out that an uncertain economic outlook is hampering the demand forecast, but long-term drivers should remain strong.

However, CommercialEdge indicated that producer prices continue to increase. If this continues, it could be problematic for the industrial sector. “Producers saddled with higher costs for goods and services are much less likely to sign new leases or renewals with increases,” the CommercialEdge analysts noted. “At a time when firms are looking to reduce costs, increases in input prices could lead to a reduction in real estate costs.”