National CRE News In Your Inbox.

Sign up for Connect emails to stay informed with CRE stories that are 150 words or less.

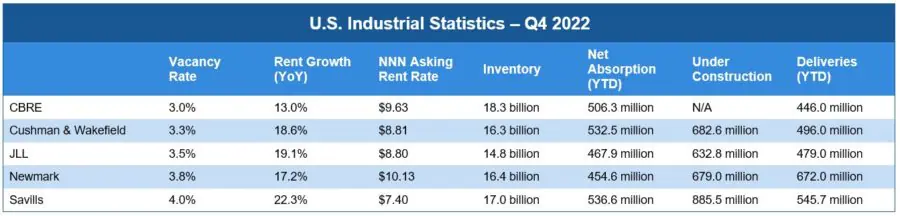

Q4 Industrial: Construction Slowing, Equilibrium Likely in 2023

During the past couple of years, the industrial real estate market was marked by record levels of absorption, construction deliveries and asking rents. On the other hands, vacancies continued to decline.

But most of the Q4 2022 market reports indicated that these trends are likely to reverse themselves in the coming year, and beyond.

Though absorption rates and deliveries remained high in Q4, “some developers opted to delay groundbreakings due to economic headwinds, and as the financing of some projects became tougher to secure,” according to Cushman & Wakefield’s MarketBeat U.S. National Industrial Q4 2022. Still, demand was plentiful due to supply chain resiliency. Commented CBRE’s U.S. Industrial Q4 2022 Report: “Companies tapped multiple ports of entry, used more onshore manufacturing and hired third-party logistics providers to lower supply chain costs and protect against import disruptions.”

Speaking of 3PL, JLL’s Q4 Industrial Outlook pointed out that retailers, especially, have outsourcing logistics and distribution operations to third parties. “While e-commerce has accounted for a high percentage of industrial leasing over the last two years, we are starting to see demand diversify amongst other industries such as Logistics & Distribution, 3PL, Construction Materials & Building Fixtures, Traditional Retailers, and Food & Beverage,” the report’s analysts said.

Savills’ U.S. Industrial Market Update, Q4 2022 noted that, even with leasing activity slowing, “the market remains historically tight,” with recent rent growth anticipated to moderate.

Most brokerage and analytics firms anticipate that the high number of new construction deliveries will likely lead to vacancy rate increases in 2023. JLL analysts said that absorption figures likely won’t change, due to delivery of pre-leased buildings. Even so, “pre-leasing rates will likely remain tepid as users navigate a turbulent macroeconomic environment and take their time when making decisions,” JLL added.

Still, demand isn’t going anywhere in the next year, with CBRE anticipating that lower inflation, continued solid retail sales and a resilient job market should keep demand for industrial product strong in 2023. Savills’ analysts agreed, pointing out that the ongoing reshoring trend means “manufacturers will stay in overdrive.”

Newmark’s 4Q22 National Industrial Market: Conditions & Trends report views the slowing construction pipeline as things getting back to normal. Said Newmark analysts: “with the construction pipeline escalating to meet burgeoning demand over the last two years and consumer spending softening, vacancy is expected to rise from the historic lows experienced in 2022 as the market recalibrates to equilibrium.”

Savills’ researchers believe that the moderating market conditions could put industrial occupiers in a better conditions. “Expect to see rents stabilizing and more flexible deal terms, including landlord concessions,” they said.

- ◦Lease

- ◦Development

- ◦Economy